Home Insurance Too Expensive to Carry in Buffalo

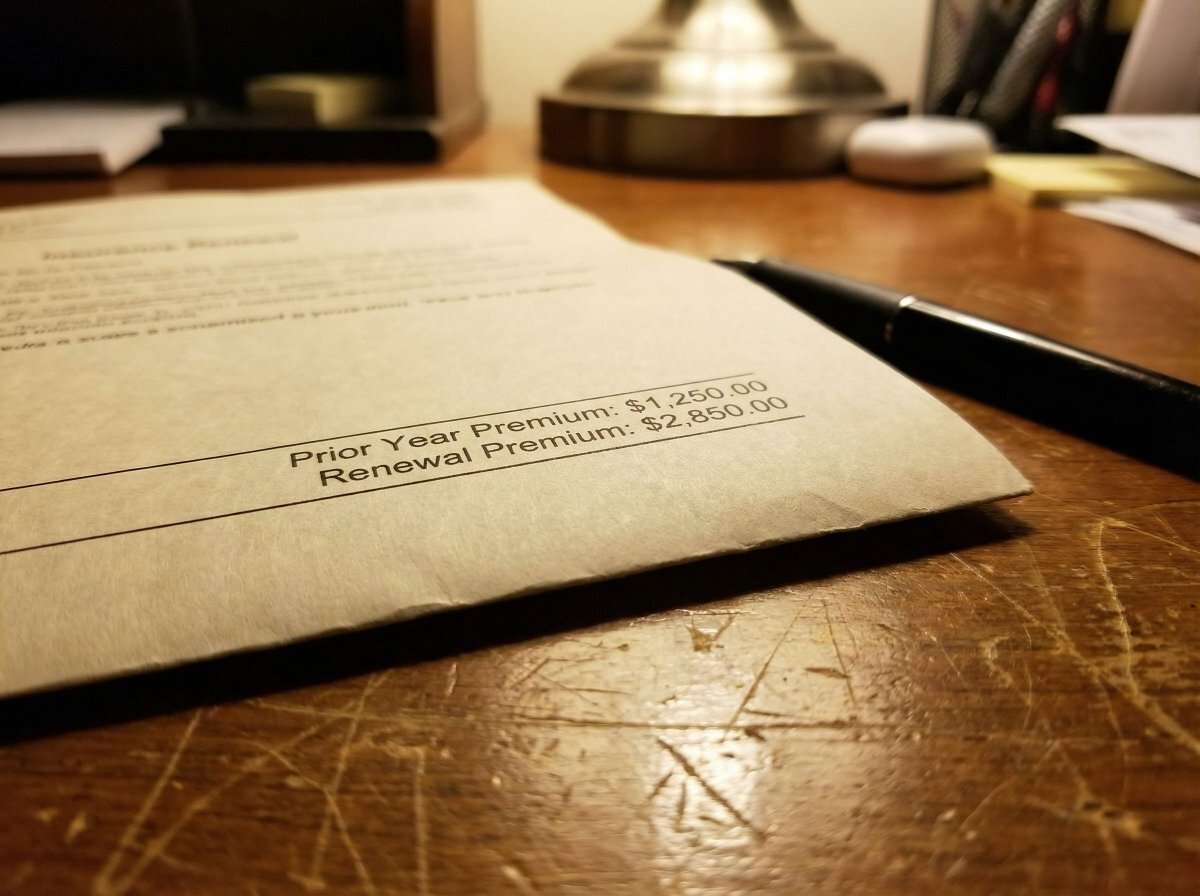

The renewal came in $2,000 higher than last year. Or the NY Fair Plan quote is the only option you could get and it’s $4,500 a year on a house worth $140,000. At some point the insurance cost stops making financial sense — and in WNY, that math is becoming a lot more common.

What’s Actually Happening

When the Premium Costs More Than the House Can Support

There’s a specific financial breaking point that WNY homeowners hit with insurance — and it doesn’t announce itself with a denial letter. It arrives as a renewal notice. The premium climbed again. The property has been claims-free for five years but the CLUE report from the prior owner is still active on the address. The carrier revaluated the replacement cost upward and the rate followed. The roof got flagged in an inspection and the policy was re-underwritten at a higher risk tier. Whatever the cause, the annual number is now a problem.

In Western New York, where most housing stock is 60–100 years old and the climate creates legitimate underwriting exposure — lake-effect snow, ice dams, freeze-thaw cycles, summer hail — insurance costs have been climbing faster than home values in many neighborhoods. A postwar ranch in Cheektowaga or a pre-war two-family on the East Side that was insurable at $900 a year a decade ago might be at $2,200 now, or on the Fair Plan at $4,500. When the insurance cost represents 3–4% of the property’s value annually, the economics of holding the property start to break down.

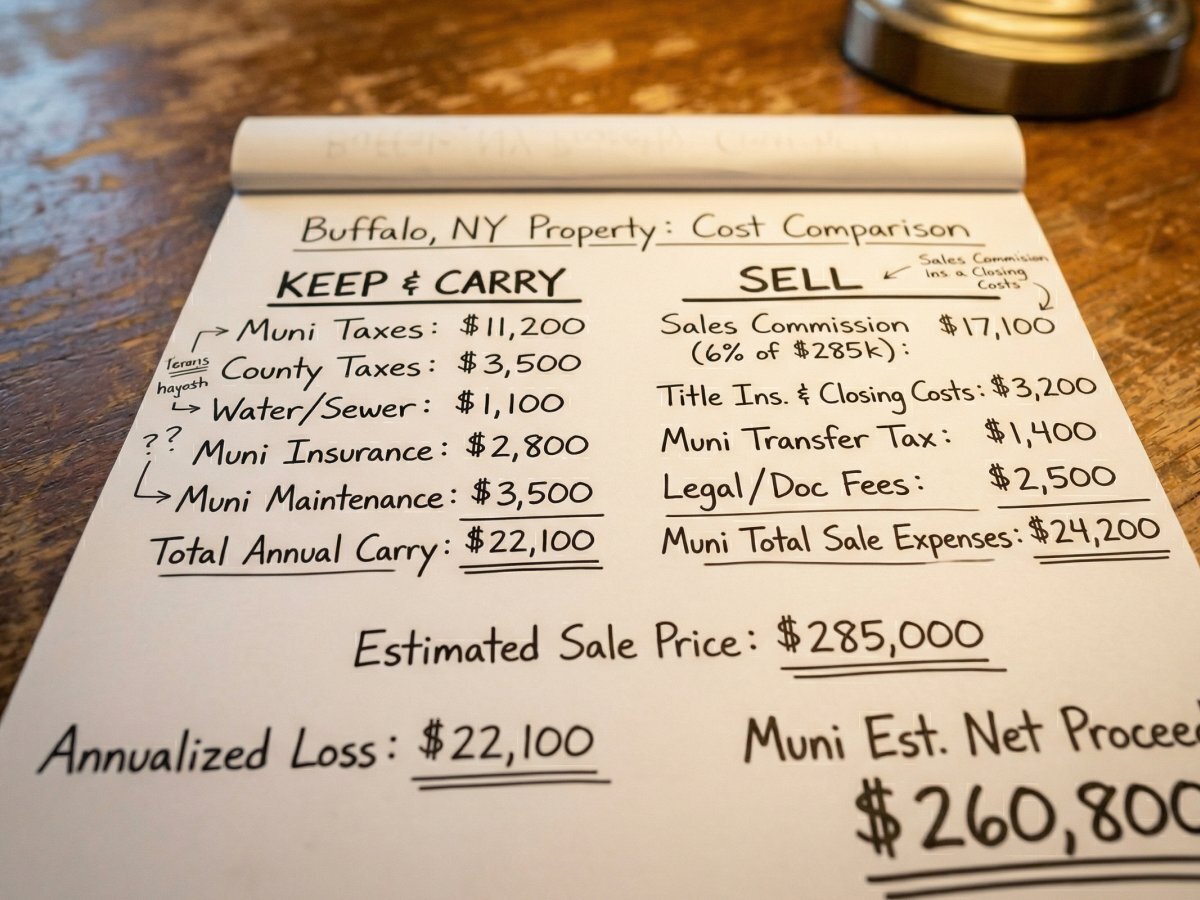

A cash sale ends the premium on a defined date. There’s no agent commission, no repair requirement, no months on market carrying that cost while the property sits. For many WNY homeowners at this crossroads, that comparison — run honestly with all the carrying costs included — looks very different than it did before they did the math.

If the premium spike came after a specific claim or series of claims, the multiple claims cost guide breaks down exactly how surcharges compound over a five-year period in WNY and when paying out of pocket on smaller losses makes more financial sense than filing. The CLUE report guide explains how the seven-year loss history attached to your address affects every carrier that quotes the property — including ones you haven’t tried yet.

If the renewal increase was driven by the carrier revaluing your home’s replacement cost, that’s a separate issue from claims history — and the renewal increase guide walks through how to challenge a replacement cost revaluation and what the options actually are in the current WNY insurance market.

Four Reasons WNY Premiums Keep Climbing

None of these require you to have filed a claim — and none of them are easy to reverse once they’re in your file.

CLUE Report on the Address

The Comprehensive Loss Underwriting Exchange tracks claims by property address — not just by owner — for seven years. If the previous owner filed two water damage claims and a fire claim, that history follows the address to you. Every carrier that quotes the property sees it. It drives up premiums, limits market options, and in some cases pushes properties to the Fair Plan before the new owner has ever filed a claim. See our CLUE report guide for the full picture on how to pull your property’s report and what can be done about it.

Replacement Cost Revaluation

Carriers periodically recalculate the estimated cost to rebuild your home from scratch — and in WNY, where contractor labor and material costs have climbed significantly since 2020, those revaluations have been pushing insured values up sharply. Higher insured value means higher premium, even if the market value of the property hasn’t moved. On a postwar ranch in Depew or Tonawanda, the gap between market value and replacement cost can be significant enough that the insurance math stops making sense.

Claims Surcharge Stacking

Most NY insurers apply surcharges after a claim — typically for three to five years. File two claims in that window and the surcharges stack. A water damage claim followed by a roof claim two years later can double a premium before the first surcharge expires. Many WNY homeowners in this situation don’t realize the surcharges are compounding until the third or fourth renewal. See our multiple claims guide for the actual math on how this compounds over time.

Risk Tier Reclassification

An insurer’s underwriting criteria change over time — and properties that were acceptable risks five years ago may now sit in higher-cost tiers based on updated models for WNY weather exposure, neighborhood loss ratios, or property age. A pre-war East Side property that was acceptable to a standard carrier at $1,100/year in 2019 might now be quoted at $2,800 by the same carrier, or not offered renewal at all. The property didn’t change. The carrier’s risk appetite did.

Premium Increase

Premium Increase

The Cost Comparison

The Cost Comparison

Premium Ends at Closing

Premium Ends at Closing

Go Deeper

More on High Insurance Costs in Buffalo

CLUE Report & High Premiums

How the seven-year claims database follows your WNY address and compounds premium increases with each additional claim.

Read Guide →Renewal Increase

Why WNY renewal premiums spike — carrier rate increases, replacement cost revaluations, inspection findings on older housing stock.

Read Guide →Multiple Claims Raised My Premium

Real math on how surcharges compound over five years in WNY — and when paying out of pocket beats filing.

Read Guide →Sell With Unaffordable Insurance

Fair Plan at $4,500/yr, surplus market, or no coverage — how a cash sale ends the premium on a defined date.

Read Guide →Common Questions

High Insurance Premium FAQ — Buffalo NY

My insurance renewal came in 40% higher than last year with no new claims. Why does that happen?

Three things drive unexplained renewal increases on WNY properties. First, carriers recalculate replacement cost annually — and with contractor labor and material costs up significantly since 2020, estimated rebuild values for Erie County homes have climbed, pulling premiums with them. Second, your carrier may have updated its risk models for WNY specifically, adjusting for increased weather-related loss exposure or neighborhood claim frequency. Third, the property may have been re-tiered based on an inspection finding you weren’t notified about. All of these can spike a renewal without any new claim activity on your part. You can request a written explanation from your carrier under NY Insurance Law §3425 and challenge a replacement cost revaluation by getting your own appraisal.

What is the NY Fair Plan and what does it actually cost for a Buffalo property?

The New York Property Insurance Underwriting Association — Fair Plan — is the insurer of last resort for properties the standard market won’t cover. For a typical WNY single-family home, Fair Plan premiums run $3,000–$5,500 per year depending on the property’s age, condition, and location. Coverage is more limited than standard HO-3 — it’s essentially fire and extended perils without the liability and personal property coverage of a full homeowner’s policy. For a Cheektowaga ranch assessed at $140,000, a $4,500 Fair Plan premium represents more than 3% of value annually — a carrying cost that compounds fast on a property that’s already difficult to sell through conventional channels.

Can I sell my Buffalo home if the only insurance I can get is the NY Fair Plan?

Yes. Fair Plan coverage satisfies the insurance requirement for a financed buyer — it’s a recognized insurer in NY. The issue is whether the buyer’s lender accepts Fair Plan coverage on the specific property. Some conventional lenders will; others require standard market coverage. FHA and VA loans have their own requirements. If the property’s condition is driving the Fair Plan situation — aging roof, deferred maintenance, prior claims — those same conditions may trigger repair requirements from the buyer’s appraiser anyway. A cash buyer sidesteps the lender’s insurance requirement entirely and prices the property condition into the offer.

How does the CLUE report affect my insurance costs and how long does it follow my address?

The Comprehensive Loss Underwriting Exchange logs claims by property address for seven years. That history is visible to every insurer that quotes the property — including carriers you’ve never had a policy with. If the prior owner filed a water damage claim and a theft claim, those show up when you try to get coverage. Carriers use the CLUE report to assess risk before quoting, and a claims-heavy address gets priced accordingly — or declined entirely. You can pull a free CLUE report on any address you own through LexisNexis at personalreports.lexisnexis.com. The report doesn’t go away until the seven-year window expires, but you can dispute inaccurate entries.

Does selling as-is to a cash buyer make more financial sense than carrying expensive insurance?

Run the actual numbers before assuming the answer. If you’re carrying $4,200/year in Fair Plan premiums on a property worth $155,000, that’s $350/month just in insurance. Add property taxes, utilities on a vacant or underused property, and any deferred maintenance costs. Then factor in what a traditional sale nets after agent commissions (5–6% in Erie County), repair demands, and carrying costs during the listing period. Many WNY homeowners who do this math find the gap between a cash offer and a traditional sale net is much smaller than they expected — and the cash sale timeline is weeks instead of months.

My insurer raised my premium after I filed a claim. Is that legal in New York?

Yes — post-claim surcharges are permitted under NY law and are standard practice. Most carriers apply a surcharge for three to five years after a paid claim. The surcharge amount depends on the type and severity of the claim — a water damage claim typically carries a higher surcharge than a theft claim. Under NY Insurance Law §2344, insurers must file their surcharge schedules with the DFS, which means the schedule is public. If you believe a surcharge was applied incorrectly or outside the filed schedule, you can file a DFS complaint. More commonly though, the surcharge is applied correctly — the question is whether it makes sense to keep the property through the full surcharge window.

Does NCB buy Buffalo homes where the insurance situation makes a conventional sale impossible?

Yes — this is one of the most common situations we see. Fair Plan coverage that a buyer’s lender won’t accept, premium costs that make carrying the property financially painful, CLUE reports that block standard market coverage on the address. We’ve purchased properties in Hamburg, Lancaster, and the Lovejoy neighborhood in Buffalo where the insurance situation made a conventional sale functionally impossible. We don’t need the property insured, we don’t have a lender, and the premium ends on the day we close — which is a specific date you pick.

Related Insurance & Financial Guides

We Buy High-Insurance-Cost Properties Throughout Western New York

Buffalo • Cheektowaga • Tonawanda • Amherst • Lackawanna • West Seneca • Hamburg • Lancaster • Depew • Kenmore • Lockport • Niagara Falls • North Tonawanda • Grand Island • Orchard Park • Sell As-Is in Buffalo

Nickel City Buyers — Buying High-Cost Insurance Properties in Buffalo & WNY Since 2013

Nickel City Buyers, LLC has been purchasing properties with unaffordable insurance, Fair Plan coverage, CLUE-flagged addresses, and surplus market situations across Erie County and Niagara County since 2013. We are a local Buffalo LLC at 3842 Harlem Rd STE 400-339, Cheektowaga, NY 14215. (716) 557-7005. 300+ homes purchased. 32 five-star Google reviews. A+ BBB. Postwar Cheektowaga ranches with replacement cost revaluations, pre-war East Side two-families with claims-heavy CLUE histories, Hamburg and Lancaster properties priced out of the standard market — the premium ends the day we close.

The Math Changes When You Include All the Carrying Costs

No obligation — a direct conversation about your Buffalo property and what a cash sale actually nets versus holding it.