Two Roads.

One Destroys

Everything.

Buffalo and Western New York homeowners facing foreclosure have more options than they realize. Understanding the difference between a short sale and a foreclosure could save your credit, your dignity, and years of your financial future. This guide covers everything — with numbers, charts, and WNY-specific facts nobody else is telling you.

Short Sale vs. Foreclosure:

What Is the Actual Difference?

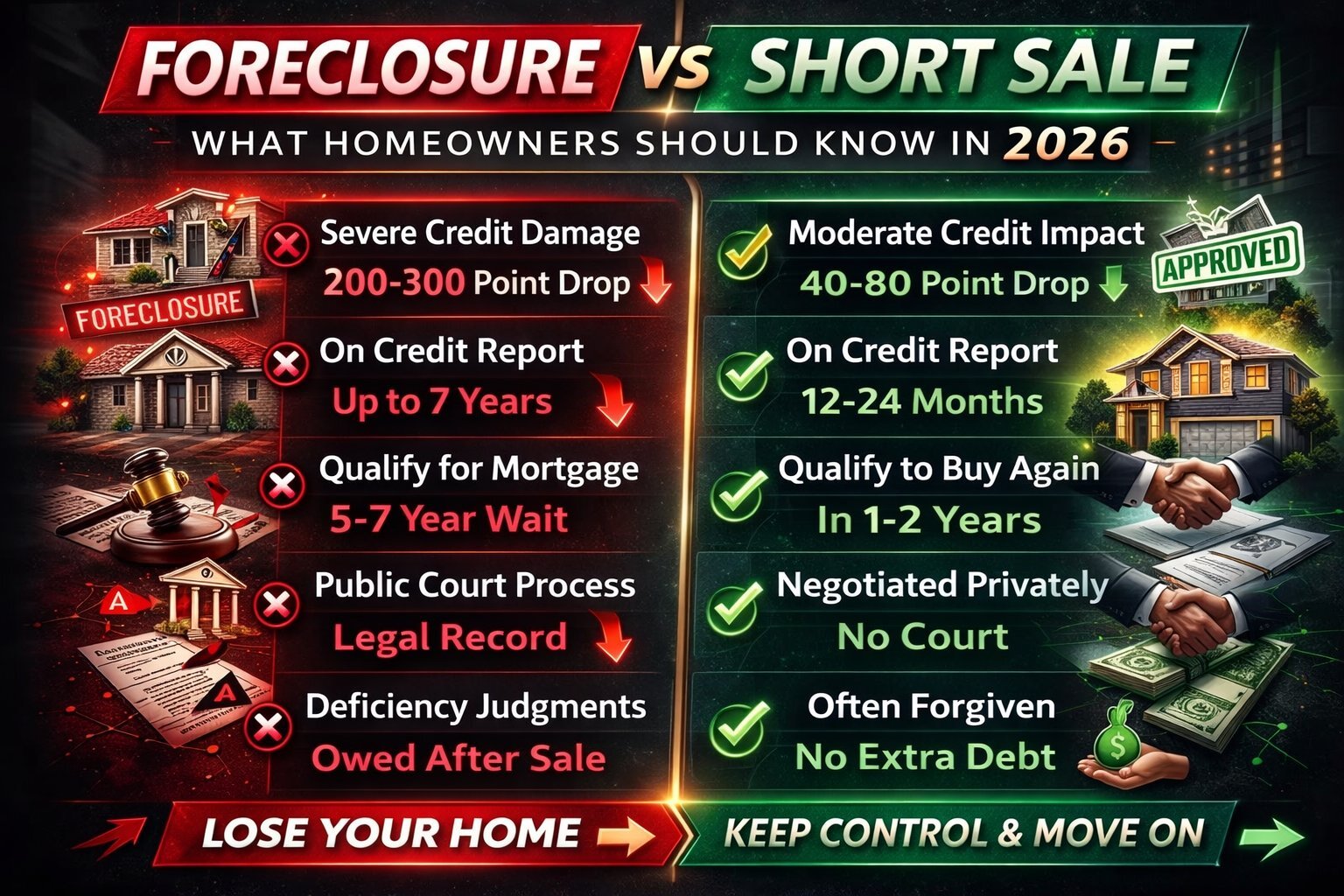

Foreclosure is what happens when you stop making mortgage payments and your lender goes to court to take the property. In New York State — a judicial foreclosure state — the bank must file a lawsuit, obtain a judgment, and schedule a public auction known as a Sheriff Sale.

You have no control. The timeline is set by the courts. The sale price is set by the auction. Erie County Sheriff Sales happen at 92 Franklin St in Buffalo. Niagara County Sheriff Sales happen at 175 Hawley St in Lockport. Once the gavel falls, it’s over.

The foreclosure appears on your credit report for 7 years. You typically walk away with zero equity and maximum credit damage. A deficiency judgment may follow you for the difference between the auction price and what you owed.

A short sale is a negotiated transaction where your lender agrees to accept less than the full mortgage balance in order to avoid the cost and uncertainty of foreclosure. You and your lender agree on a sale price — typically below what you owe — and the property is sold to a buyer.

You have control. You choose to initiate it. You negotiate the terms. The sale is private — not a public auction. No Sheriff, no courthouse steps, no public record of loss in Erie or Niagara County court.

Credit impact is significantly lower — typically 40-80 points versus 200-300 for a completed foreclosure. You can often qualify for a new mortgage in 1-2 years versus 5-7 after foreclosure. In many cases the lender forgives the deficiency entirely.

Foreclosure vs. Short Sale:

What Buffalo Homeowners Should Know in 2026

How Much Does Each Option

Damage Your Credit Score?

How Long Does Each Path Take

in Erie and Niagara County?

Every Factor That Matters to Buffalo

and WNY Homeowners in 2026

Foreclosure vs. Short Sale vs. Cash Sale

— Every Variable Compared

| Factor | 🔴 Foreclosure | 🟢 Short Sale | ⭐ Cash Sale — NCB |

|---|---|---|---|

| Credit Score Impact | 200–300 point drop | 80–150 point drop | Minimal — standard sale |

| Stays on Credit Report | 7 years | 12–24 months typically | Does not appear as foreclosure |

| Time to Complete | 12–24 months (NY courts) | 60–120 days | 7–21 days |

| Next Mortgage Eligibility | 5–7 years wait | 1–2 years wait | Fastest path to rebuild |

| Public Record | Yes — Erie/Niagara County court | No — private transaction | No — private transaction |

| Deficiency Judgment Risk | High — bank can pursue you | Often forgiven in negotiation | Eliminated at closing |

| Equity Received | Typically none | None — bank takes all | Yes — above payoff amount |

| Control Over Timeline | None — court controlled | Partial — lender must approve | Full — you choose close date |

| Repairs Required | Irrelevant — bank takes as-is | Negotiable | None — we buy as-is |

| Agent Commissions | N/A | Often required — reduces net | None — we pay all closing costs |

| Emotional Stress Level | Extreme — months of uncertainty | Moderate — lender negotiations | Lowest — clean, fast, private |

| Overall Verdict | ❌ Worst outcome | ⚠️ Better — if time allows | ✅ Best for most WNY sellers |

The NCB Short Sale Process in New York State

When a cash sale isn’t possible because you owe more than the property is worth, a short sale facilitated by Nickel City Buyers is the next best option for Buffalo and WNY homeowners. Here’s exactly how it works — from first call to closed deal.

Years Until Your Next Mortgage

After Each Outcome

This is the number most Buffalo homeowners never consider until it’s too late. How long before you can own a home again?

Fannie Mae requires a 7-year waiting period after foreclosure before a conventional mortgage. FHA requires 3 years minimum. VA requires 2 years. Rentals may be denied for years due to the public record in Erie or Niagara County court.

Conventional loans typically require a 2–4 year waiting period after a short sale depending on the loan type and down payment. FHA and VA have shorter windows. You can rebuild credit and reenter the market far sooner than post-foreclosure.

Selling to Nickel City Buyers before default records as a standard real estate transaction. No foreclosure flag. No waiting period triggered. You can pursue new housing immediately — rent or purchase — without the cloud of foreclosure following you.

New York State Foreclosure Facts

Every Erie & Niagara County Homeowner Must Know

Unlike many states where foreclosure can happen in as little as 90 days, New York requires a full court process. The bank must file a lawsuit, serve you, obtain a judgment, and schedule a Sheriff Sale. This timeline — typically 12 to 24 months — gives WNY homeowners significantly more time to act than most people realize.

New York State law requires lenders to send a 90-day pre-foreclosure notice before filing any foreclosure action. This mandatory notice period is your window of maximum options. A cash sale can be completed entirely within this 90-day window — before any court filing, before any public record.

Once your lender files a Lis Pendens in Erie County Supreme Court or Niagara County Supreme Court, the foreclosure becomes a public record visible to anyone. Neighbors, employers, and future landlords can see it. A short sale or cash sale completed before Lis Pendens filing keeps your situation entirely private.

New York State does not provide a post-sale redemption period for residential foreclosures. Once the Erie County or Niagara County Sheriff Sale is completed, you cannot buy the property back. This makes acting before the sale date absolutely critical — there is no second chance after the gavel falls.

Western New York has one of the oldest housing inventories in the United States — a significant percentage of Buffalo, Cheektowaga, Lackawanna, and Niagara Falls homes were built before 1950. Older homes require constant maintenance investment. When life circumstances change, the carrying cost of an older WNY home accelerates financial distress faster than national averages.

After a foreclosure, if the Erie or Niagara County Sheriff Sale doesn’t generate enough to cover your full mortgage balance, your lender can pursue you personally for the difference — called a deficiency judgment. New York courts enforce these. Short sale negotiations often include deficiency waiver as part of the agreement. Cash sales eliminate the issue entirely.

- Sheriff Sale Location: 92 Franklin St, Buffalo NY 14202

- Administering Office: Erie County Sheriff’s Office

- Court: Erie County Supreme Court

- Filing Record: Erie County Clerk’s Office

- Official Resource: erie.gov/sheriff

- Sales publicly listed — visible to anyone searching your address

- Erie County has one of NY’s highest foreclosure inventory rates

- Post-war housing stock in Cheektowaga, Lackawanna, Tonawanda most at risk

- Sheriff Sale Location: 175 Hawley St, Lockport NY 14094

- Administering Office: Niagara County Sheriff’s Office

- Court: Niagara County Supreme Court

- Filing Record: Niagara County Clerk’s Office

- Official Resource: niagara-county.org/sheriff

- Niagara Falls has among WNY’s highest foreclosure rates per capita

- Sales publicly listed — visible to neighbors and employers

- Older Niagara Falls and Lockport housing stock creates elevated distress

The WNY Homeowner Decision Matrix —

6 Real Situations

Sold. Clean.

Moving Forward.

Hundreds of Buffalo and Western New York homeowners have chosen the cash sale path with Nickel City Buyers — avoiding foreclosure, protecting their credit, and walking away with cash in hand instead of a court judgment. This is what the right outcome looks like.

Get My Cash Offer →We Know Buffalo. We Know Erie County.

We Know Niagara County.

Every national “we buy houses” company treats Buffalo like it’s Phoenix or Atlanta. We were born in WNY, we’ve bought 300+ homes here since 2013, and we know the difference between a Cheektowaga bungalow and a Lockport colonial — and what each one is actually worth.

300+ homes purchased across Erie and Niagara County. We’ve been buying WNY homes since before Shamrock existed. We know every zip code, every neighborhood, every quirk of the local market.

No bank financing. No contingencies. No waiting. We close on your timeline — which can be as fast as 48 hours if there’s a Sheriff Sale pending in Erie or Niagara County.

We buy houses in any condition across WNY — fire damage, code violations, hoarder situations, decades of deferred maintenance. You walk away. We handle everything after closing.

No agent commission. No closing costs. No hidden fees. What we offer is what you receive at closing. We even pay back taxes and outstanding liens from the sale proceeds.

No open houses. No MLS listing. No neighbors knowing your business. No public record of financial distress. A cash sale to NCB is completely private — just like it should be.

33 verified reviews from real WNY sellers. A+ Better Business Bureau rating. We’ve been building our reputation in Buffalo one home at a time since 2013 — not a national franchise.

Free Guide — 5 Ways to Stop or Avoid Foreclosure in WNY

Not ready to call? Download our free guide — covers every option for Buffalo and Erie/Niagara County homeowners.

Short Sale vs. Foreclosure —

Buffalo NY FAQ

What is the difference between a short sale and a foreclosure in Buffalo NY?

A short sale is a voluntary, negotiated transaction where your Buffalo lender agrees to accept less than the full mortgage balance in order to avoid foreclosure. You initiate it, negotiate the terms, and complete a private real estate transaction. A foreclosure is an involuntary court process where your lender sues you in Erie or Niagara County Supreme Court, obtains a judgment, and sells your property at a public Sheriff Sale — at 92 Franklin St in Buffalo or 175 Hawley St in Lockport. A short sale leaves you with far less credit damage and no public court record. A foreclosure destroys your credit for 7 years and is visible in public court records permanently.

How much does a foreclosure damage your credit score compared to a short sale in New York?

A completed foreclosure typically causes a credit score drop of 200–300 points and remains on your credit report for 7 years under New York State reporting rules. A short sale typically causes a drop of 80–150 points and may clear from your report in 12–24 months depending on how it is reported by the lender. A cash sale to Nickel City Buyers before default records as a standard real estate transaction — it does not trigger a foreclosure flag and causes minimal credit impact.

How long after a foreclosure in Erie County before I can buy a house again?

After a completed Erie County foreclosure, Fannie Mae guidelines require a 7-year waiting period before you can qualify for a conventional mortgage. FHA requires a minimum of 3 years. VA loans require 2 years. After a short sale, conventional loan waiting periods are typically 2–4 years depending on the loan type and your down payment amount. After a cash sale before default, there is no waiting period triggered — you can pursue new housing immediately.

Can Nickel City Buyers help with a short sale in Buffalo or Niagara County?

Yes. When a homeowner owes more than the property is worth — making a direct cash sale impossible — we can facilitate a short sale with your lender. We work with Erie County and Niagara County properties and understand the local lender landscape. The short sale process requires lender approval and typically takes 60–120 days. If your auction date is imminent, a cash sale may be the only viable option — call us immediately at (716) 557-7005 to discuss your specific situation.

What happens if my Buffalo home sells for less than I owe at a Sheriff Sale?

If your Erie County or Niagara County property sells at Sheriff Sale for less than your outstanding mortgage balance, your lender may pursue you personally for the difference through a deficiency judgment in New York State court. New York law allows lenders to seek deficiency judgments, and courts enforce them. This means even after losing your home at auction, you could still owe tens of thousands of dollars. Short sale negotiations often include a lender agreement to waive deficiency as part of the deal. A cash sale eliminates this risk entirely — all liens are paid at closing.

Is a short sale better than foreclosure for Buffalo homeowners?

In almost every measurable way, yes. A short sale results in less credit damage, a shorter credit recovery period, no public court record, and often includes a deficiency waiver from your lender. The primary disadvantage is time — short sales typically require 60–120 days and lender cooperation. If your Niagara or Erie County auction date is within weeks, a short sale may not be feasible. In that case, a cash sale to Nickel City Buyers is the fastest path to stopping the foreclosure before it completes.

How does New York State foreclosure law affect Buffalo homeowners differently than other states?

New York is a judicial foreclosure state — one of the most homeowner-protective in the country. Your lender must go through Erie County or Niagara County Supreme Court before your property can be sold. This process typically takes 12–24 months from first missed payment to Sheriff Sale. You are also entitled to a mandatory 90-day pre-foreclosure notice period before any court action can begin. This extended timeline gives Buffalo and WNY homeowners significantly more opportunity to act — pursue a short sale, negotiate with the lender, or sell to a cash buyer — than homeowners in non-judicial states.

What are the short sale vs foreclosure options for Niagara County homeowners?

Niagara County homeowners have the same options as Erie County homeowners under New York State law. Niagara County foreclosures proceed through Niagara County Supreme Court and result in a Sheriff Sale at the Niagara County Courthouse, 175 Hawley Street in Lockport. The same 90-day pre-foreclosure notice requirement applies. Short sales in Niagara County require lender approval and typically take 60–120 days. We buy pre-foreclosure and foreclosure properties throughout Niagara County — Niagara Falls, Lockport, North Tonawanda, Lewiston, Youngstown, Wheatfield, Pendleton, and Newfane. Call (716) 557-7005.

Can I do a short sale if I already have a foreclosure date scheduled in Buffalo?

Possibly — but it depends on how much time remains. A short sale requires your lender to agree, review the offer, and approve the transaction. This process typically takes 60–120 days minimum. If your Erie County or Niagara County Sheriff Sale is within that window, a short sale is unlikely to close in time. A cash sale to Nickel City Buyers — which can close in as little as 48 hours — is the more viable option when the auction date is set. Call us immediately if you have a scheduled auction date: (716) 557-7005.

Nickel City Buyers — Short Sale & Foreclosure Experts Serving Buffalo, Erie County & Niagara County Since 2013

Nickel City Buyers, LLC is a local cash home buyer specializing in short sales and pre-foreclosure purchases throughout Western New York. We help homeowners understand and navigate the difference between short sale and foreclosure — and close fast cash sales before Sheriff Sale dates in Erie and Niagara County. Located at 3842 Harlem Rd STE 400-339, Cheektowaga, NY 14215. Phone: (716) 557-7005. Website: nickelcitybuyers.com. Erie County Sheriff Sales at 92 Franklin St, Buffalo NY 14202. Niagara County Sheriff Sales at 175 Hawley St, Lockport NY 14094. We serve Buffalo, Cheektowaga, Tonawanda, Amherst, Lackawanna, West Seneca, Hamburg, Orchard Park, Lancaster, Depew, Kenmore, Williamsville, East Aurora, Clarence, Akron, Grand Island, East Amherst, Colden, Niagara Falls, Lockport, North Tonawanda, Lewiston, Youngstown, Wheatfield, Pendleton, Newfane, Wilson, and all surrounding Erie and Niagara County communities. A+ BBB rating. 5.0 stars Google. 300+ homes purchased since 2013. Stop Foreclosure → | All Situations → | All Areas →

Foreclosure Takes Everything.

We Give You a Way Out.

You now know the difference. You know the numbers. You know what foreclosure costs in Buffalo and Western New York — in credit, in time, in equity. The next move is yours. One call starts the process.